How is the war in Ukraine affecting inflation around the world? Who is actually paying for it? And how much? Why do developing countries such as China, India and Saudi Arabia, which have not yet joined the sanctions against the invading country, the aggressor of the war in Ukraine, end up paying more?

Apart from the suffering and the humanitarian crisis caused by the invasion of Ukraine, the whole world economy has felt the effect of the decrease in the rate of growth and rapid inflation. The depreciation of one currency creates consequences for that country. But what if all currencies in the world depreciate simultaneously? What effect will it have on the countries where this inflation seems to be moderate?

Global inflation in 2022 increased to 8.7%, and according to the forecasts, , this index in 2023 will be as high as 6.8%. More than two-thirds of this record high inflation falls on energy resources and food products [1].

However, in the event of the depreciation of all world currencies, it is the money and savings that is bound to these currencies, such as deposits and monetary bonds, that depreciate the most.

In regions of Europe and Central Asia, in the developing markets, the inflation in 2022 was 15.9%, which is the highest index for over 20 years and the highest among all developing regions of the world.

According to the BP statistical data, before the war, Russia extracted 12% of the world’s oil, out of which it consumed just over 3% and exported about 9% to the other countries. The gas extraction was 17% of the world output, out of which the national consumption was 12%, and sales to other countries were 5% [2].

And according to the IEA energy agency report, in 2022 Russia exported almost the same amount of oil having changed the buyers. And the export of gas decreased by 20%, i.e., from 5% to 4% of the world’s extraction.

Why has the world reduction in gas output of 1% and the change in the structure of the buyers of Russian oil resulted in the outrageous increase in the price of energy resources (up to 83%), food products (up to 48%), and the global inflation of 8.7%? One of the studies published by FRS states that the fear and uncertainty unjustifiable war of Russia against Ukraine and the risk of war spreading is a separate cause of inflation [7].

Moreover, according to the forecasts of the IE agency, the export of Russian gas in 2023 will fall by another 15%, and the export of oil will fall only by 10%. This means that the export of oil and gas will fall by less than 1% globally in 2023, and global inflation will grow by 6.8%, and up to 16% in the developing markets. Why does fear and uncertainty induce the inflation more than a shortage of certain goods?

After money became paper and electronic, there has been nothing behind the money but the promise of the states[8]. Promises of what? – The State promise to control the situation and that tomorrow there will be a certain order, protection of rights, including property rights.

The crime of Russia against the borders of the sovereign state of Ukraine, acknowledged by absolutely all countries of the world and the simultaneous disregard of sanctions by certain leading countries of the world, create disappointment the order of the future and the protection of property rights in general.

When there is distrust in the future order, manufacturers are forced to place an additional reserve on the price of their goods and services, raising prices. The less confidence in societal order and protection of rights, the greater the reserve, the greater the prices.

The people, corporations, and states that have assets in the currency, deposits or bonds suffer the losses caused by inflation, and not only the inflation of currency in which these assets are kept, but global inflation, since it affects the real value of their assets.

So who are the biggest holder of assets expressed in money that suffers the losses caused by the global (total) inflation?

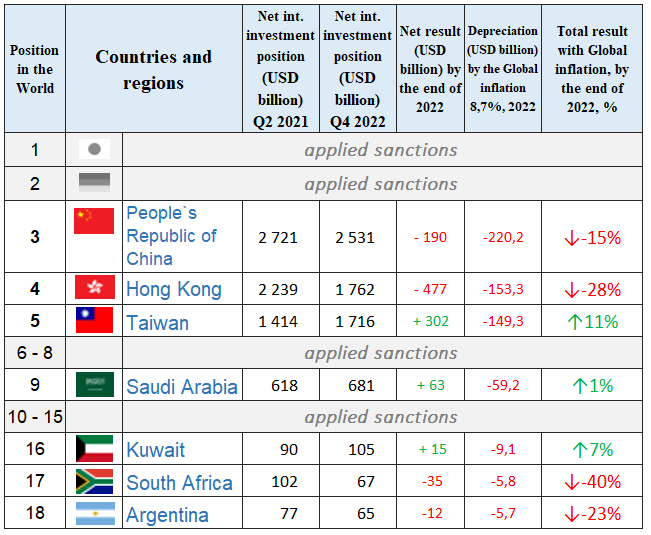

According to the UN Report, in 2022, the world state debts reached a record-high of 90 trillion USD[9]. However, each borrowing state is also a money lender. It is important to consider in which currency the loan was received and the currency in which it was lent. The difference between the borrowing and lending is a country’s net investment position. Thus, according to the open sources, the crediting countries include many countries that either did not join the sanctions and even some that took a neutral position.

Therefore, the treat of losing a substantial amount of profit due to global inflation among the states that did not fully comply with the sanctions is the highest [10]:

The sovereign investing states. by a long way, are not the only investors keeping their savings bound to the currencies. Private investors lend money to the banks, and in many countries, the pension funds invest their money in securities or bonds.

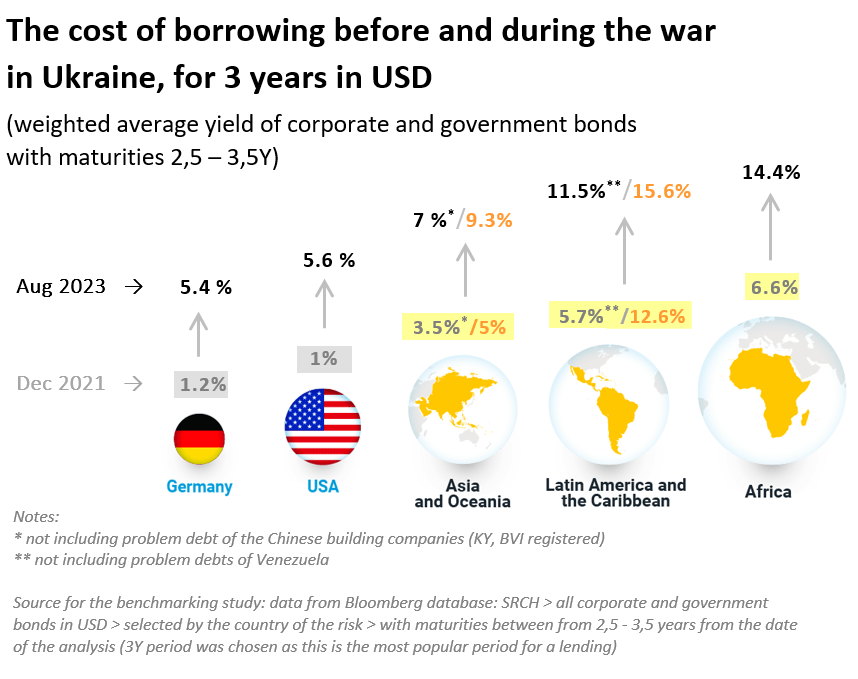

At the beginning of war, understanding the inevitable wave of inflation, and, consequently, the dissatisfaction of creditors, with the beginning of war all leading countries started to consider compensating for future inflation in the loan pricing by increasing the interest rates of loans.

In this case, the creditors receive the high interest rate covering the inflation before they receive their money back from their debtors.

Central banks of all leading world countries increased the key interest rates to a 30-50 year record level.

In principle, the increase of rates is the transfer from creditors to borrowers of losses caused by the reduction of confidence in states due to the inability to stop the war.

However, such a transfer would not be uniform, since even before the war the loan pricing in the world was not uniform and depended upon the country and the level of the debtor’s risk. The increase of the loan pricing for the developing countries and the businesses in these countries reached an unprecedentedly high level:

According to the UN Report, about 3.3 bn people now live in countries where the debt interests exceed the expenses for healthcare or education[9].

Due to russia’s war against Ukraine, the world’s inflation and, consequently, the growth of the debt burden prevent the countries from investing in sustainable development and green energy.

Will the people’s confidence in states and their currencies in general be regained if Ukraine returns its territories only militarily (and this will definitely happen) without the support of sanctions by Asia, Africa, and South America?

Is the return of confidence in the legal system possible if the criminal is half-condemned and it has not paid for the damages?

If most countries that now maintain neutrality purchase or trade Russian oil and gas do not join sanctions, the confidence in the countries’ and currency’s capacity in general will not be fully regained even after the military victory of Ukraine.

The high inflation without the extension of sanctions will remain even after the war.

And, in contrast to this, joining sanctions against the Russian oil and gas, Russian military production will reinforce confidence in the legal system of the world and will reduce inflation based on fear.

Will the cost of energy resources grow in case of a more substantial embargo on the Russian resources? Yes, they will, but the countries and companies not burning their income in the kettle of war but investing in the economy will receive super-high income. Each large modern energy company be it Aramco, ExxonMobil, Shell, or British Petroleum, have their own projects in green energy.

Moreover, if inflation is caused by a shortage of essential goods, such inflation has the bottom – inflation will slow down if the loses connected with the shortage are distributed.

But when will inflation, interest rates rising, and a decrease in GDP, which are based on a fear and mistrust of states, stop?

Inflation based on fear without harming GDP will stop after reducing the grounds for fear – after increasing domestic production of weapons, which is now a decisive factor in war, and after energy and economic readiness for war. Weapon is in the first place because there is no point in a power plant if a transformer is on fire because a missile hit it.

Can the countries not joining the sanctions count on the support of the other countries through sanctions in case of unjustified, unveiled, military offense against them in the future? Such countries will have to invest more in weapons and the GDP of such countries, although it might be similar to growth, will be very far from the one expected by the citizens of such countries.

Joining sanctions by countries such as China, India, Saudi Arabia, Qatar, Brazil, South Africa will mean not only the reduction of inflation and loan pricing, this will be the entrance of the club by the countries that are capable of controlling the situation not being governed by the temporary advantages awaiting that the other country will be the following country in some absolutely unjustifiable war.

Joining the sanctions against russia by the countries that are themselves under sanctions (such as Saudi Arabia) apart from the capability to control will mean the transfer to an absolutely new level of respect for the supremacy of law. The acknowledgment of other crimes, even if you consider the accusations against yourself unfair, underlines the coolness of judgment which is even more important, since no conflict in the world is the last conflict ever.

Sources:

- The World Bank: Russia’s Invasion of Ukraine and Cost-of-Living Crisis Dim Growth Prospects in Emerging Europe and Central Asia, April 6, 2023, https://www.worldbank.org/en/news/press-release/2023/04/06/russian-invasion-of-ukraine-and-cost-of-living-crisis-dim-growth-prospects-in-emerging-europe-and-central-asia

- BP: Statistical Review of World Energy 2022 | 71st edition https://www.bp.com/content/dam/bp/business-sites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2022-full-report.pdf

- FT: Global inflation tracker: see how your country compares on rising prices https://www.ft.com/content/088d3368-bb8b-4ff3-9df7-a7680d4d81b2

- IEA: Russian total oil exports, January 2022 – January 2022, 22 Feb 2023 https://www.iea.org/data-and-statistics/charts/russian-total-oil-exports-january-2022-january-2023

- IEA: Russian gas exports in the World Energy Outlook 2022 vs. 2021 Russian gas exports in the World Energy Outlook 2022 vs. 2021 – Charts – Data & Statistics – IEA

- Forbs: BP Energy Outlook 2023: War Accelerates Oil And Gas Decline, Instability Pushes Renewables To 60%, Russian Energy Takes A Hit, Feb 16, 2023https://www.forbes.com/sites/ianpalmer/2023/02/16/bp-energy-outlook-2023-war-accelerates-oil-and-gas-decline-instability-pushes-renewables-to-60-russian-energy-takes-a-hit/?sh=106a1aa26b40

- FEDS Notes: The Effect of the War in Ukraine on Global Activity and Inflation, May 27, 2022, https://www.federalreserve.gov/econres/notes/feds-notes/the-effect-of-the-war-in-ukraine-on-global-activity-and-inflation-20220527.html

- Dmitry Kalinichenko: Закон Грешема – это нелепая ошибка или умышленная подмена понятий и передергивание фактов? Часть II https://www.kdggold.com/ru/content/zakon-greshema-eto-nelepaya-oshibka-ili-umyshlennaya-podmena-ponyatij-i-peredergivanie-faktov-chast-ii-zakon-rublya/

- UN GLOBAL CRISIS RESPONSE GROUP: A world of debt: A growing burden to global prosperity, July 2023, https://unctad.org/publication/world-of-debt

- CEIC: Net International Investment Position https://www.ceicdata.com/en/indicator/net-international-investment-position

Leave a comment